Small business owners often struggle to find affordable financing for major purchases. SBA 504 loans offer fixed-rate, long-term financing for real estate and equipment. This article explores current SBA 504 loan rates and their historical trends. Understanding these rates can help businesses make smart borrowing decisions.

Key Takeaways of SBA 504 Loan Current Rates

- SBA 504 loan rates as of September 2024 are 5.76% for 25-year terms, 5.83% for 20-year terms, and 5.87% for 10-year terms.

- Rates have varied over recent years, with 2020 seeing very low rates (sometimes under 2.5%) due to economic conditions, while 2023 experienced higher rates, peaking at 7.18% for 20-year loans in October.

- Fixed rates of SBA 504 loans provide stability for long-term planning, shielding businesses from market fluctuations and allowing for accurate budget forecasting.

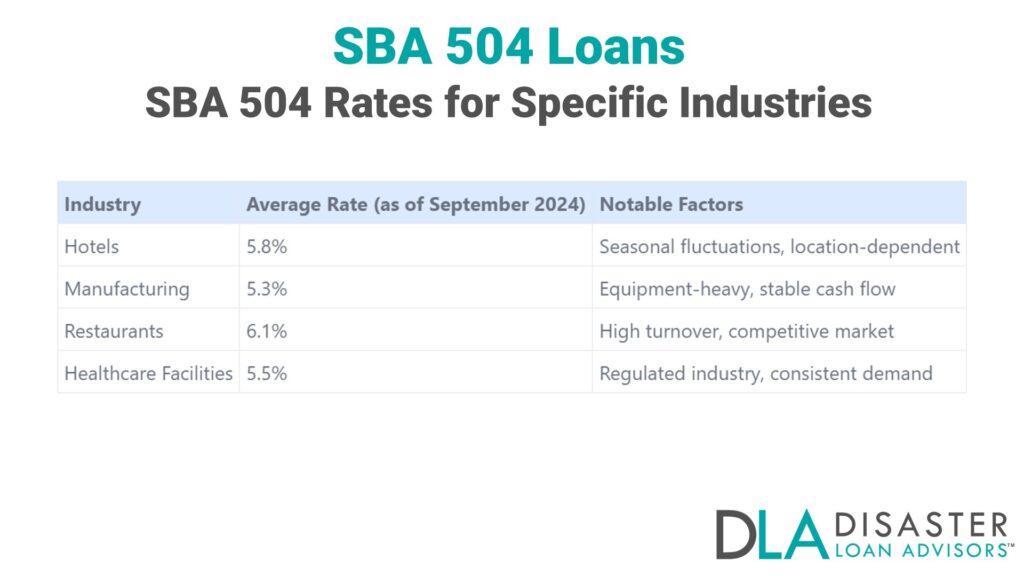

- Different industries may receive varying rates, with hotels averaging 5.8%, manufacturing 5.3%, restaurants 6.1%, and healthcare facilities 5.5% as of September 2024.

- Experts predict SBA 504 loan rates will remain relatively stable through 2025, based on Federal Reserve policies and current economic conditions.

Current SBA 504 Loan Rates

SBA 504 loan rates are now at 5.75% for 20-year loans and 5.85% for 25-year loans. These rates show a slight drop from last month, giving small businesses a chance to save on long-term financing costs.

Rates as of September 2024

SBA 504 loan rates as of September 2024 offer attractive options for business owners. The 25-year term boasts a 5.76% interest rate, while the 20-year term sits at 5.83%. For those seeking shorter commitments, the 10-year term comes in at 5.87%. These fixed rates provide stability and predictability for long-term financial planning.

Business owners can benefit from these competitive rates when financing fixed assets. The U.S. Small Business Administration backs these loans, making them a solid choice for growth and expansion. Certified Development Companies (CDCs) work with lenders to process these loans, ensuring a smooth application process for qualified borrowers.

Comparison with Previous Years

SBA 504 loan rates have varied over the years, reflecting economic conditions. A comparison with previous years shows certain patterns:

2023 experienced high rates across different loan terms:

- 10-Year loans reached 7.06% in July

- 20-Year loans hit 7.18% in October

- 25-Year loans peaked at 7.13% in October

2022 rates were generally lower than 2023 highs:

- 10-Year loans averaged around 5.5%

- 20-Year loans were near 5.7%

- 25-Year loans typically stayed below 5.9%

2021 offered more advantageous rates for borrowers:

- 10-Year loans often fell between 2.8% and 3.5%

- 20-Year loans ranged from 3.0% to 3.8%

- 25-Year loans usually remained under 4.0%

2020 had very low rates due to economic circumstances:

- 10-Year loans decreased to 2.2% in some months

- 20-Year loans reached very low levels, occasionally below 2.5%

- 25-Year loans offered excellent value, sometimes under 2.7%

These comparisons show the significance of timing in securing SBA 504 loans. Disaster Loan Advisors (DLA) can assist businesses in understanding these rate changes for optimal financing decisions.

Historical Trends in SBA 504 Loan Rates

SBA 504 loan rates have seen ups and downs over the past few years. From 2020 to 2024, these rates changed in ways that affected many small businesses.

Analysis from 2020 to 2024

SBA 504 loan rates have changed a lot from 2020 to 2024. Let’s look at the key trends and shifts during this period:

- 2020 started with higher rates but ended lower. The 20-year loans began at 3.629% in January and dropped to 2.427% by December.

- Early 2021 saw low rates continue. The 10-year loans started at 2.254%, while 20-year loans were at 2.496%.

- 2022 marked a sharp rise in rates. The 10-year loans jumped from 3.07% in January to 6.53% in December.

- Economic factors played a big role in rate changes. The U.S. Treasury benchmarks and other market forces affected the rates.

- The COVID-19 pandemic impacted rates in 2020 and 2021. The low rates helped many small businesses during tough times.

- 2023 and 2024 saw rates level off. After the big jumps in 2022, the rates became more stable.

- Different loan terms showed varied trends. The 10-year and 20-year loans often moved in similar patterns, but not always.

- The Certified Development Company (CDC) loan program adapted to these changes. They worked to keep loans available to small businesses.

- Job creation remained a key goal of the SBA 504 program. Even with rate changes, the focus on helping businesses grow stayed strong.

- The fixed-rate nature of SBA 504 loans proved valuable. It gave business owners more certainty in their long-term planning.

Significant changes and their impacts

SBA 504 loan rates experienced significant changes from 2022 to 2023. In 2022, the 10-year loan rate increased from 3.07% to 6.53%. This substantial increase made borrowing more expensive for small businesses.

The pattern continued into 2023, with rates reaching even higher levels. July 2023 saw the 10-year rate reach 7.06%, while October brought 20-year and 25-year rates to 7.18% and 7.13% respectively.

These shifts considerably affected small business financing. Higher rates resulted in larger monthly payments for borrowers. Some companies had to reconsider their expansion plans or explore alternative funding sources.

Nevertheless, the fixed nature of SBA 504 rates still provided stability compared to variable-rate loans. Companies that secured lower rates before the increases benefited from a cost advantage over competitors who borrowed later.

Factors Influencing SBA 504 Loan Rates

SBA 504 loan rates don’t exist in a vacuum. They respond to shifts in U.S. Treasury benchmarks and key economic indicators.

U.S. Treasury benchmarks

U.S. Treasury benchmarks play a key role in setting SBA 504 loan rates. These benchmarks, like the 5-year and 10-year Treasury notes, serve as a base for lenders to calculate interest rates. As Treasury yields rise or fall, SBA 504 rates often follow suit.

The link between Treasury benchmarks and SBA 504 rates helps small businesses plan for loans. Lenders use these benchmarks to offer competitive rates while managing risk. This system allows the Small Business Administration to provide stable, long-term financing options for growing companies.

Economic indicatorsEconomic indicators shape SBA 504 loan rates. These markers, such as GDP growth, inflation, and job reports, provide lenders with a view of the economy’s health. The Federal Reserve monitors these signs to set monetary policy, which directly affects loan rates. From 2020 to 2022, a combination of low interest rates and strong economic recovery resulted in a steady increase in SBA 504 rates.

Market trends and business cycles also influence loan rates. During periods of economic expansion, rates tend to rise as demand for loans grows. Conversely, in slower periods, rates may decrease to encourage borrowing and boost growth. Small business owners should monitor these patterns to make informed decisions about when to apply for an SBA 504 loan.

Benefits of Fixed Rate SBA 504 Loans

Fixed rate SBA 504 loans offer stability in a changing market. Borrowers can plan their finances with confidence, knowing their payments won’t rise unexpectedly.

Long-term financial planning

SBA 504 loans provide a strong basis for long-term financial planning. These loans feature fixed interest rates over 10, 20, or 25 years. This consistency enables business owners to forecast their monthly payments accurately. They can budget confidently, knowing their loan costs will remain constant over time.

The fixed rates of SBA 504 loans shield businesses from market fluctuations. If interest rates increase, SBA 504 borrowers retain their lower rate. This feature assists companies in managing cash flow and planning for expansion. With consistent payments, owners can concentrate on operating their business rather than concerning themselves with changing loan terms.

Stability in repayment terms

SBA 504 loans provide consistent repayment terms that assist businesses in better financial planning. These loans feature fixed interest rates, ensuring monthly payments remain constant throughout the loan’s duration.

This consistency allows owners to budget more precisely and avoid unexpected changes in rates. It’s particularly beneficial for small businesses that need to carefully manage their cash flow.

Fixed rates also safeguard borrowers from market fluctuations. If interest rates increase, SBA 504 loan holders maintain their lower rate. This can result in substantial savings over time, especially for long-term loans. The consistent payments enable businesses to expand and invest in other areas without concerns about increasing loan expenses.

SBA 504 Rates for Specific Industries (e. g. , Hotels)

SBA 504 loan rates differ across industries, with hotels serving as a notable example. These rates reflect the specific characteristics and risks associated with each sector.

Hotels often encounter specific challenges in securing financing. The industry’s cyclical nature and sensitivity to economic changes affect loan rates. Location is a key factor in determining risk levels for hotel projects.

Manufacturing businesses typically receive lower rates due to their asset-heavy nature. The stability of equipment as collateral often results in more favorable terms. Cash flow consistency in this sector also contributes to better rates.

Restaurants face higher rates because of their high failure rates and intense competition. Lenders consider this industry riskier, leading to slightly elevated interest rates. However, established restaurants with proven track records may secure better terms.

Healthcare facilities benefit from the essential nature of their services. The consistent demand for medical care translates to more stable revenue streams. This stability often leads to more attractive loan rates for healthcare projects.

Disaster Loan Advisors (DLA) assists businesses in understanding these industry-specific rates. They provide guidance on securing the most favorable terms based on each sector’s specific characteristics.

Karl and Kurt Hughes demonstrate successful use of SBA 504 loans in the hospitality industry. They secured a historic location for their brewery, using the program’s benefits for their specific needs.

Butch Grimm’s case shows the program’s adaptability across industries. His success in reducing payments by $30,000 and accessing $1 million in working capital displays the potential benefits for various sectors.

Crepini’s relocation illustrates how the program adapts to different industry needs. Their move to a larger facility using SBA 504 financing demonstrates the program’s flexibility across sectors.

Knowing these industry-specific rates helps businesses make informed decisions. It allows them to compare their options effectively and choose the most suitable financing solution for their needs.

How SBA 504 Rates Compare to Other SBA Loan Programs

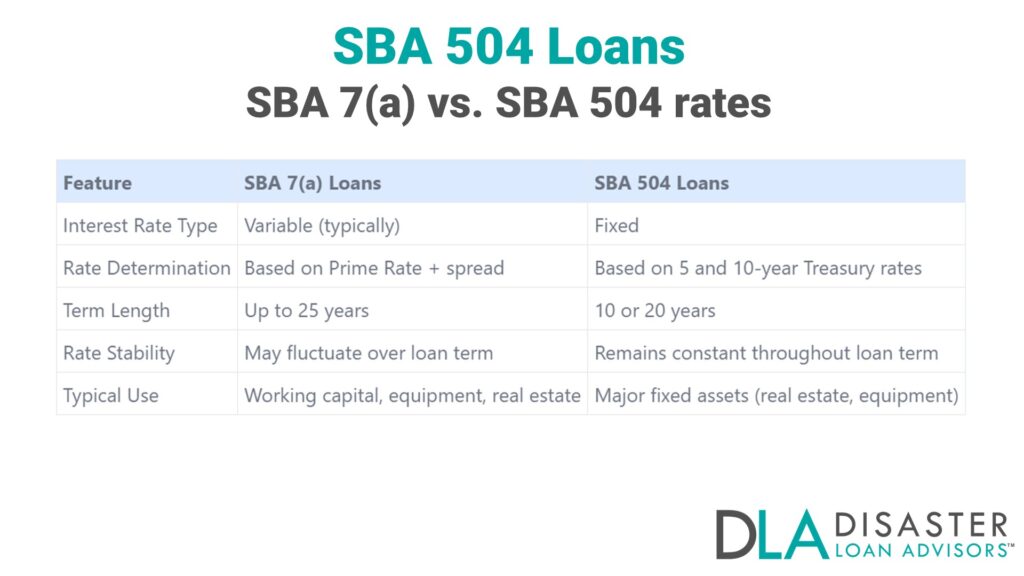

SBA 504 loans offer lower rates than SBA 7(a) loans for fixed asset financing. Businesses can save money with SBA 504’s fixed rates, which stay the same over the loan’s life.

SBA 7(a) vs. SBA 504 rates

SBA 7(a) and SBA 504 loans offer different rate structures for small business owners. Understanding these differences helps entrepreneurs make informed financing decisions.

SBA 504 loans provide fixed rates below market prices. This feature allows for steady, predictable payments over the loan’s life. In contrast, SBA 7(a) loans often have variable rates, which can change based on market conditions.

Business owners seeking long-term financing for major assets often prefer SBA 504 loans. The fixed rate structure helps with financial planning and budgeting. SBA 7(a) loans, while more flexible in use, carry the risk of rate increases over time.

Both loan programs serve distinct purposes. SBA 504 loans excel in fixed asset financing, while SBA 7(a) loans offer versatility for various business needs. Entrepreneurs should consider their specific requirements and risk tolerance when choosing between these options.

Disaster Loan Advisors (DLA) can provide guidance on selecting the appropriate SBA loan program. Their knowledge assists business owners with loan applications and terms.

Advantages of SBA 504 for fixed asset financing

SBA 504 loans shine for fixed asset financing. They offer low, fixed interest rates that stay the same over time. This helps business owners plan their budgets with more ease. The loans also let owners keep more cash on hand. They only need to put down 10% of the project cost, which is less than most other loans ask for.

These loans work well for buying land, buildings, or heavy equipment. They can cover up to 90% of the project cost. This means owners can save their money for other business needs. Plus, if a business qualifies, it can turn equity into working capital through refinancing. This feature gives owners more options to grow their business over time.

Future Predictions for SBA 504 Loan Rates

Economic analysts anticipate SBA 504 loan rates will remain low through 2025. This projection is based on the Federal Reserve’s monetary policy and the general economic conditions.

Expert opinions

Financial experts monitor SBA 504 loan rates carefully. They examine market trends and economic data to make informed predictions about future rates. Many professionals expect rates to remain stable in the short term. This perspective is based on the Federal Reserve’s current position on interest rates.

Some analysts forecast a minor increase in rates by the end of the year. They base this on projected economic growth and inflation targets. Nevertheless, most agree that any rises will likely be gradual. Business owners should stay informed about these expert predictions. They can assist with planning for future borrowing requirements.

Economic forecasts affecting ratesEconomic projections influence SBA 504 loan rates. Analysts consider factors such as inflation, employment growth, and GDP when making assessments. These forecasts assist lenders and borrowers in preparing for potential rate adjustments. For instance, if inflation is anticipated to increase, loan rates might follow suit.

The U.S. Treasury benchmarks also affect SBA 504 rates. These benchmarks indicate the overall economic condition. During periods of economic strength, rates typically increase. In slower economic times, rates often decrease to stimulate borrowing and growth. Small business owners should monitor these patterns to make informed financing decisions.

Frequently Asked Questions About SBA 504 Loan Current Rates

1. What Are SBA 504 Loan Current Rates?

SBA 504 loan current rates are interest rates set by the Small Business Administration for long-term, fixed-rate financing. These rates change monthly based on market conditions. The Central Servicing Agent handles the debentures that fund these loans.

2. How Does My Credit Score Affect My SBA 504 Loan?

Your credit score plays a big role in your loan approval. Lenders look at your creditworthiness during underwriting. A higher score often means better rates and terms. But don’t worry – there’s more to it than just numbers.

3. Can I Use an SBA 504 Loan for Business Growth?

Yes, SBA 504 loans are great for business growth. You can use them to buy land, buildings, or equipment. They’re perfect for expanding your operations or even buying a new building. Just remember, you’ll need to put some of your own money in too.

4. What’s The Difference Between A First Mortgage and an SBA 504 Loan?

A first mortgage is typically from a bank and covers 50% of the project cost. The SBA 504 loan, arranged by a Certified Development Company (CDC), covers up to 40%. You pay the rest. This setup helps spread the risk and makes it easier for small businesses to get financed.

5. Do I Need Title Insurance for an SBA 504 Loan?

Yes, you’ll need title insurance. It protects you and the lender if there are issues with property ownership. It’s a standard part of the process – like paying taxes or checking your account balance.

Conclusion and Summary of SBA 504 Loan Current Rates: Stay Informed on Trends

SBA 504 loans offer a solid option for small business owners seeking fixed-asset financing. These loans provide competitive rates and long-term stability. Business owners can benefit from the program’s low down payments and fixed interest rates.

The SBA 504 loan program has proven its value in supporting economic growth across the U.S. As rates continue to evolve, staying informed about current trends will help businesses make smart financial choices.

Invest in Your Business with the SBA 504 Loan Program: Affordable Long-Term Financing for Big Opportunities!

The SBA 504 Loan Program is the ultimate solution for small business owners ready to make long-term investments in their growth. Whether you’re planning to purchase commercial real estate, upgrade facilities, or acquire essential equipment, this program offers the tools to achieve your goals with unmatched affordability and flexibility.

With the SBA 504 Loan Program, you can:

- Secure Fixed, Below-Market Interest Rates for predictable payments over time.

- Access Up to $5.5 Million for real estate, equipment, or major improvements.

- Benefit from Long Repayment Terms of 10, 20, or 25 years to ease cash flow.

- Enjoy Low Down Payments typically just 10%, allowing you to preserve working capital.

Unlike traditional loans, SBA 504 Loans focus on helping small business owners invest in their future with terms that prioritize sustainability and growth.

Eligible Uses for SBA 504 Loans:

- Purchasing or constructing owner-occupied commercial real estate

- Acquiring heavy machinery or large equipment

- Renovating or modernizing facilities

- Refinancing existing debt tied to eligible projects

Don’t Let Business Financing Hold You Back. Take the Next Step Today!Want to discuss if an SBA 504 Loan is the right option for your small business? Schedule Your Free Consultation to see how we can help.

Cover Image Credit: 123RF.com / Serezniy. Illustration Credit: Disaster Loan Advisors (DLA).

As a leading dedicated member of the Tax and Accounting Team at Disaster Loan Advisors™, Mark focuses on unlocking the ERC Tax Credit's potential for eligible firms that qualify, providing strategic advice, and detailed guidance to ensure substantial financial recovery and growth. His methodical approach to client engagement includes comprehensive deep-dive analysis, customized consultation and guidance, and a commitment to achieving tangible results for each business served.

Disaster Loan Advisors™ (DLA) offers a comprehensive suite of services designed to navigate the complexities of the Employee Retention Tax Credit (ERC) program, ensuring that qualified businesses leverage the maximum possible benefit with minimum hassle. Unlike some firms that charge exorbitant contingency or percentage-based fees (often between 10% to 30% of your ERC refund), DLA operates on a fair and reasonable, transparent flat-fee structure that aligns with the IRS's guidelines.

If you are looking for an ERC Company that believes in providing professional ERC Services and value for small business owners, in exchange for a fair, reasonable, and ethical fee for the amount of work required, Disaster Loan Advisors™ is a good fit for you. STAY SAFE. STAY COMPLIANT. KEEP MORE OF YOUR REFUND.™

- SBA 7a Loans for Healthcare and Medical Businesses - January 26, 2025

- SBA 7a Loans for Non-Profit Organizations - January 25, 2025

- Interest Rate Caps of SBA 7a Loans - January 24, 2025